Do you have a clear idea of what a financial advisor does? Should you hire a financial advisor? What should be your selection criteria? Are you a high net worth individual? What is an appropriate fee? These are the matters that will be addressed in this blog.

This blog is primarily aimed at retirees or pre-retirees with investible assets of $1m or more (high net worth individual, HNWI) but it will also apply to many with $500k+ of investible assets, particularly those with other sources of retirement income beyond social security. Although the target audience of this article begins with those having investments of $1m, there is no upper limit.

Where am I coming from? I am a retired international corporate tax attorney and CPA. I switched from individual planning to corporate planning early in my career. When it came time to tackle my own retirement planning, I realized I lacked the specialized knowledge to do such planning and began the process of getting educated. Over the last 10 years I have developed a comprehensive retirement financial plan for my own use, and have continued to study financial planning and the financial planning industry. I am not a financial advisor and do not aspire to become one. I have no personal financial interests served by this blog.

This blog deals with the selection of a financial advisor and financial advisor fees. There are two initial posts. The first will examine: services provided by FAs; types of clients who will benefit by hiring an FA; and criteria for selecting an FA. The second post discusses FA fees. It discusses in detail the nature and problems with current fee arrangements, and suggests how the retiree should deal with such fees.

Part 1: Services and Selection of Financial Advisors

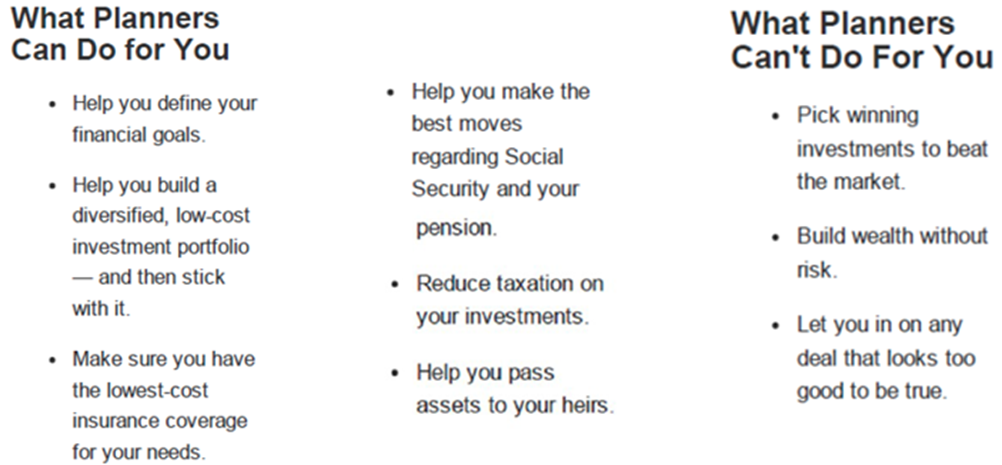

The first and perhaps the most important point relates to something that the FA cannot do -- beat the market. Many FAs will disagree and claim that beating the market is one of the most important services that they provide. Investment management is an important service of FAs, but the premise of this article is that the FA cannot pick market-beating stocks or funds. For those interested in a more detailed analysis comparing passive index funds with actively managed funds, see A Case for Index Fund Portfolios.

Some claim that they can beat the market, not by stock picking, but by building a better diversified, low-cost investment portfolio. Helping select a passive portfolio that is appropriate for the client, is an important service provided by the financial planner; however, the tweaks that financial planners make to passive investing in order to “beat the market” are of questionable value. To the extent there may be some value, such tweaking advice does not involve substantial additional time or skill.

Services of the Financial Advisor

Following are two summaries of the services provided by a FA. The first comes from this article by Allan Roth, a financial planner, How to Choose a Financial Planner.

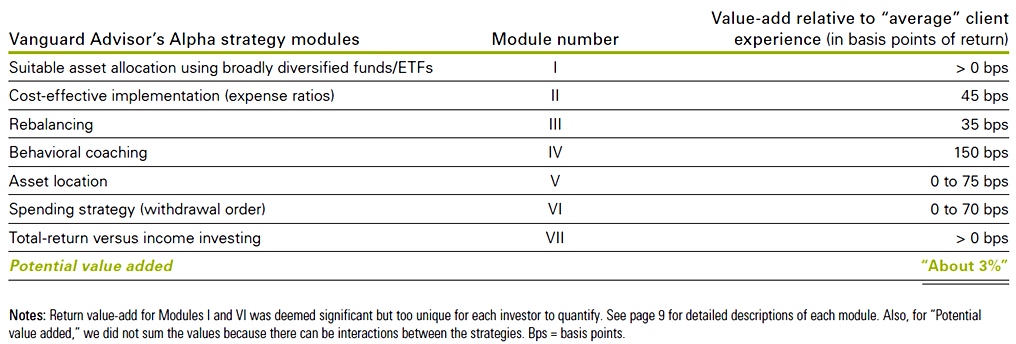

The second summary is from a study prepared by The Vanguard Group. The following schedule summarizes how various FA services can increase net returns for their clients.

Defining Financial Goals

Defining goals is an extremely important role of the FA. All planning is based upon a complete understanding of the client's financial position, his objectives and goals, and his behavioral leanings such as degree of risk aversion. The FA must synthesize all of this information to generate a realistic estimate of retirement spending both present and future, considering all goals and contingencies. The FA must obtain a complete understanding of all sources of future after-tax income, and reasonably project when and in what amounts such income will be realized. This income must then be compared and reconciled with projected needs. Such analyses must be continually updated. You will find my approach to such an analysis in my other blog and my article, Retirement Planning with Annual Available Spend.

Building the Portfolio and Sticking with it

In the financial analysis review discussed above, the FA will estimate the investment mix and expected returns. Now it will be necessary to fine tune the investments. The purpose of this is not to propose market beating investments, but to select investments that are compatible with the client's need, ability, and willingness to take risk. This is the second bullet of the Roth list and Modules I-IV in the Vanguard list. The investments must be diversified, and this is generally accomplished with a mix of index funds and/or ETFs.

Module II relates to the low cost portfolio. It contemplates low cost index funds such as those sold by Vanguard. Vanguard estimates the savings at about 0.45%. It is important to understand that the advisor fee is not the only investment-related expense. When the advisor selects mutual funds or ETFs, there are also expenses incurred by the fund/ETF. These expenses are often quite small for some index funds, e.g., 0.15%, but some of the more complex active funds have expense ratios in excess of 1%. For a good discussion of how these fees and expenses can add up, see The Heavy Toll Of Investment Fees.

Modules III and IV relate to "sticking with it". Rebalancing between fixed and equity investments is done to maintain or update the most desirable risk level as determined above. Module IV estimates that the greatest value add is from behavioral coaching, 1.5%. It is simply human nature to buy more equities when the market is soaring, and perhaps sell all when the market tanks (2008). The FA's job is to maintain sanity and the original risk objectives.

Insurance, Pensions, and Social Security

The FA will work with the client to determine the appropriate amounts of various types of insurance, and, in most cases, should consider the applicability of annuities. For many HNWIs, their assets will be sufficient to self insure, reducing the need for insurance. Planning pension distributions, required minimum distributions, Social Security benefits, etc. are also important tasks undertaken by the FA.

Income tax and Estate Planning

The FA will assist with income tax planning relative to investments such as: Module V, planning what assets should be in taxable or tax deferred accounts; and Module VI, planning asset spending in order to minimize taxation. The FA should be able to deal with these investment related tax issues, but generally, the FA is not a tax preparer, and broader income tax services will be done by the client's CPA or other tax advisor.

Estate planning and preparation of wills is generally done through an estate planning attorney. The FA will often assist in financial analysis and implementing various approaches to gifting and inheritance.

Other

The FA will often assist with a range of other financial issues: education or large purchase funding; charitable giving; beneficiary reviews, etc.

Selecting a Financial Advisor

Do You Need the Services of a FA?

Many HNWI opt to go it alone and do their own financial planning. For some, that is the right choice, but for most others, the better choice is to hire a financial advisor. If you are considering taking on your own financial planning, look closely at the description of FA services above. Are you prepared to do all of these tasks? Are you prepared to educate yourself on any matters where you are not prepared? Will you be able to recognize when you will need outside assistance? Some people handle DIY very well, but many others do not.

Note the 1.5% value impact of Module IV, behavioral coaching. A qualified FA will have the interpersonal skills to recognize and work with the client's behavioral propensities, whatever those may be. How risk averse is the client? What will he likely do if the market soars or tanks? Is the client likely to stray from his investment policy statement, and how best can he be kept on course? Of course, some people have no problem with controlling their own behavior, but several studies show how poorly many do in this regard.

How to Select a Financial Advisor

The basic criteria to consider when selecting a financial advisor include technical knowledge, personal skills, and fees. Fees will be discussed in Part 2 below. This article assumes that the retiree will hire a fee-only advisor -- an advisor who is not a stock broker or insurance agent, and who does not receive any commissions or kickbacks of any sort.

The FA should have all the requisite skills to perform the services outlined above. At a minimum the FA should be a CFP or CPA/PFS. The FA must have all the technical skills, but, as importantly, the interpersonal skills to earn the client's trust and respect when dealing with behavioral matters. Of course, reputation in the community can be valuable information when making the decision.

The websites of financial advisor firms are often not clear in identifying the types of services and specific fees that the advisor and firm will take. I highly recommend that anyone looking to hire a financial planning firm first check the SEC Investment Adviser Search (after retrieving the firm by name and clicking on “SEC” (or state), scroll down the left hand navigation panel and click on “Part 2 Brochure”. The Part 2 ADV Brochure will provide most of the details on services provided and fees.

Conclusion

Most HNWIs will benefit from the services of a financial advisor. Hiring a FA will not help the HNWI beat the market, but the FA will help his client create and maintain an investment portfolio that is appropriate to his specific situation. The FA will also perform additional services related to various other financial matters. The FA should have both the necessary technical and interpersonal skills.